I trust you were able to take some quality downtime with your family to recharge and reflect on the monumentally different year we have lived through. I wish you, your colleagues, friends, and family a healthy, safe, and fulfilled year for 2021.

I wanted to share with you my closing thoughts for 2020 in Insurtech and more broadly. I won’t focus on the blockbuster year it was for Insurtech IPOs because I’ve covered it extensively earlier. You can read more here.

Table of Contents

COVID-19 and Firing on All Engines

Before I get into the discussion of Amazon vs. the Brokers, a review of 2020 wouldn’t be complete without some focus on COVID-19. To begin with, I believe there was no better example of an insurance carrier’s ability to adapt and launch much-needed insurance products than WeSure. WeSure is Tencent’s Insurance arm. They were able to launch 4 insurance products in partnership with two traditional carriers in 4 weeks. Is there a traditional domestic carrier that could even launch 1 product in 4 months? See the figure below which highlights WeSure’s journey. This, to me, exemplifies the true art of the possible, and this is what I wish for all of us in 2021. 2021 should be the year we can get to the point where we are nimble enough to react to market needs and fill them quickly.

The Power of Data: Workers Comp Example

A second example is what ClearPrism has been able to do by uniquely pulling together public and private data to analyze the impact of Covid-19, including relevant legislation. This example is focused on the risk exposure of workers’ compensation carriers to COVID-19. For example, as we see in the diagram below, they pulled together the potential impact on the industry at the state-level of legislative action along with Covid exposure data. They also appended data on salaries and lost wages which ultimately drive some of the comp claims. This shows the true power of combining analytics with public and private data.

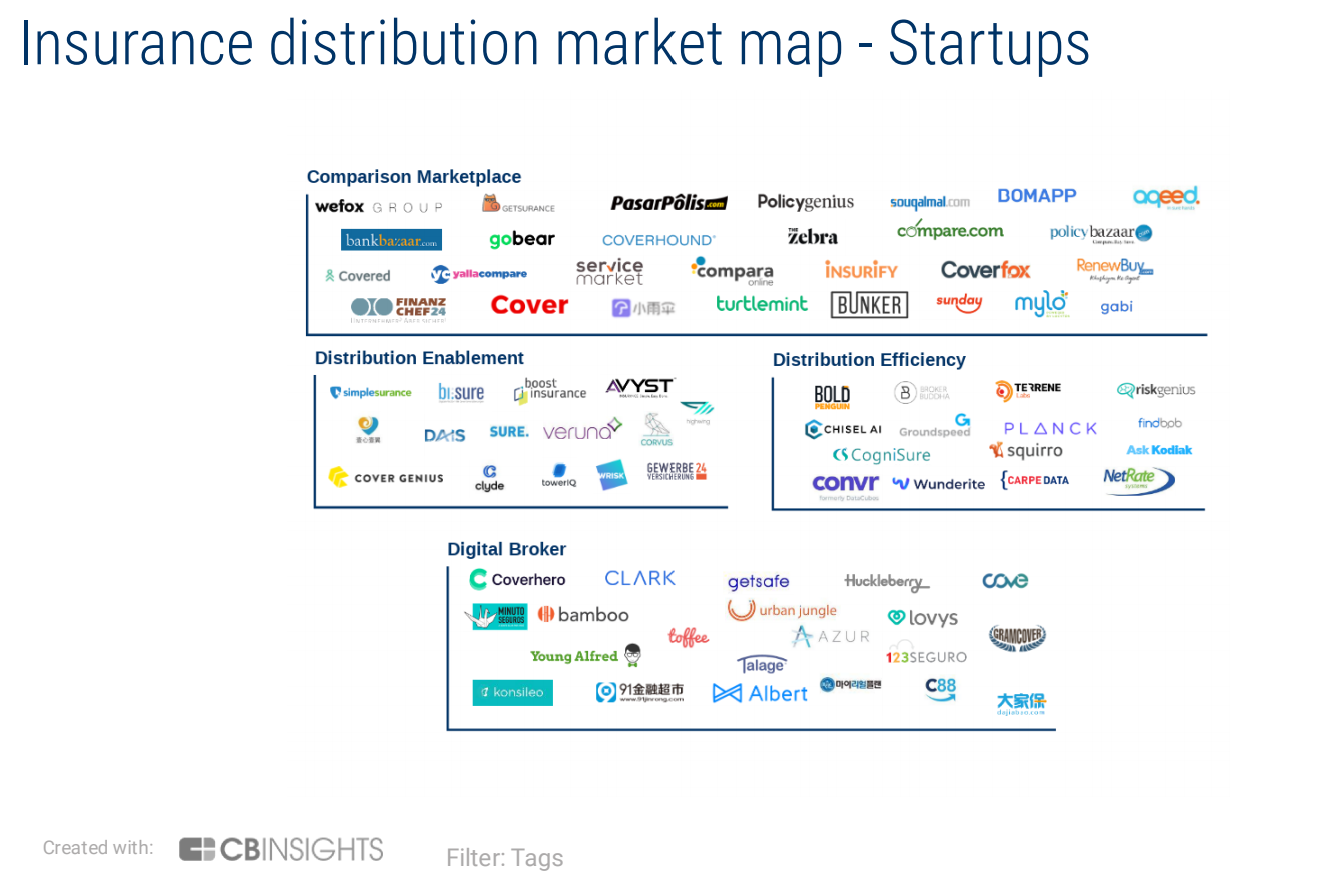

Other insurtechs have focused more on introducing the performance of external data to specific verticals or improving the customer and agent experience through prefill applications, including Insurtechs such as Planck, CarpeData and Terrene Labs, to name a few. Even independent agent-focused comparison engines such as ITC’s TurboRater and EzLynx provide prefill to simplify the process for home and car applications. Do you use external data to help your agents simplify the application process?

We will be hosting a webinar in January with Clearprism to discuss some of these findings and the potential impacts on the Industry for 2021. Please let me know if you want to be invited to the webinar.

Amazon vs the Brokers

In September, Amazon announced its 3Q revenue results of $96.1B and a trailing 12 months (TTM) revenue of $348B. To put that in context, in 2019, the entire US P&C market premiums were $637.7B. Amazon’s revenue is almost 55% of the entire P&C market. WOW!

So why is this important? It’s important because as we all know, 2020 accelerated the digital agenda. Would any of you made the transition to work from home as rapidly without COVID-19?

In fact, prior to Covid-19, it was projected that 25% of all P&C premium would be written directly through the digital channels by 2024. That’s up from 14% in 2019. I suspect this will be only higher now. Moreover, 30% of all Auto insurance was bought online in 2019 and JD Power found that for the first time, the insurance carrier’s website was more important to a consumer, than their agent (34% vs. 33%).

VCs have continued to pour money into online brokers/distribution plays, not only in Personal Lines, but they have now expanded beyond Small Commercial into Middle-Market Commercial. According to CBInsights, there was $190M of funding across 9 deals in 2020. American Insurtechs accounted for $155M of that sum, with the mostly commercial insurer Newfront Insurance bringing in the single largest investment at $100M. See the broader market map below.

Table 1 presents some high-level data on some of the digital players as well as regional brokers and the mega brokers. While these digital marketplaces have seen significant growth in revenue, the larger traditional brokers have been able to keep up. That is to be expected, because most of those digital players sell leads to agents (both captive and independent).

Table1

Who is winning: digital or traditional?

I think the answer to this question is both. While investors seem to value digital players over traditional brokers (comparing market capitalization to revenue), most of the companies listed above have seen significant growth in revenue year over year. That said, on the whole, the brokers are doing better net net compared to their online counterparts, and this is seen by the higher EBITDA margin rates.

I believe the most important conclusion we see from the above data, is that there is a symbiotic relationship between the digital players and the brokers. Brokers need the leads that these online sources provide in order to grow. The more tailored and targeted the lead, the more likely the traditional broker is to close the policy and the higher the price that can be charged for the lead.

Gone are the days of having a storefront on Main Street and being a community-based broker. This model was already struggling pre-Covid, and even more so now. Digital has become a key to survival. It doesn’t matter if you are a broker or a carrier. Covid-19 accelerated the need to become a digital-savvy player.

Suggestions for 2021

So what did we learn in 2020 that can position us to make more informed decisions in 2021? I’ve listed a few of my recommendations for 2021.

- Continue to focus on the policyholder experience while simultaneously improving the agent experience.

- Data is key, but only if you use it to improve underwriting, claims, or pricing. You not only need the data but more importantly, you need a plan and approach to integrating the new data into your operational processes.

- If you aren’t already using external data in the areas of imagery, claims, and fraud, or agent and policyholder targeting and segmentation, start NOW!

- The time is ripe to explore new distribution partnerships.

- The time is even more critical to explore creating new products or new product features/endorsements. Look to the changing market needs and consumption patterns for ideas of where to focus your attention.

I look forward to staying in touch this year. Those of you who know me more personally know I grew up in a musical family where my father, aunt, and grandparents were professional musicians. I can’t think of a more fitting recording to close out 2020 and looking towards 2021 than the following recording of Andrea Bocelli and his 8-year-old daughter. I hope you enjoy it.

Happy New Year

Kaenan

About Insurtech Advisors

Insurtech Advisors is dedicated to helping regional insurance carriers and agencies find and partner with Insurtechs enabling you to thrive and continue to meet the needs of your members and independent agents. We work closely with your team to identify opportunities and aspirations and then personally curate and introduce you to the best Insurtechs to pilot.

Kaenan is a professional in the areas of block chain, telematics, wearables, analytics, artificial intelligence (AI) and Insurtech. He has played a key role in innovating many start-ups and established carriers. His advice has been widely appreciated in the financial community, which resulted in multiple quotes and publications in various media.

Most recently he was Practice Lead for Innovation, Fintech, and Strategic Insights at EY. Throughout his career he has held leading roles within Marketing Strategy and Decision Management with top Insurance, Banking and Finance companies, including USAA, Citibank and Sallie Mae.